{kind=link}

Conventional (handbook) underwriting processes typically battle to maintain tempo with the rising complexity of contemporary threat evaluation, information assortment, and coverage administration.

🧐

Scaling conventional underwriting operations turns into more and more difficult as underwriters spend a big period of time gathering and verifying information from a number of sources.

These embody buyer functions, monetary data, medical experiences, and exterior threat assessments equivalent to geographic or weather-related information. These numerous information units require cautious aggregation and verification, making the method gradual and error-prone.

🧐

Underwriting automation might help alleviate these points to an awesome extent. It leverages AI and machine studying to shortly and precisely acquire, assess, and course of underwriting information. This not solely accelerates decision-making but in addition ensures extra correct and constant threat assessments. This additionally leads to streamlined workflows, quicker selections, and vital price reductions—by as a lot as 50% in operational bills, in line with some trade experiences!

This text focuses on what particular points of the underwriting course of might be automated, the applied sciences driving this transformation, and why this shift is so essential for contemporary insurance coverage corporations.

Key underwriting processes that may be automated

Automating key steps within the insurance coverage underwriting course of permits insurers to streamline operations, enhance accuracy, and cut back the time spent on handbook duties. Automation can remodel how underwriters work, enabling quicker and extra constant decision-making whereas minimizing human error.

Listed here are particular underwriting processes that may profit from automation:

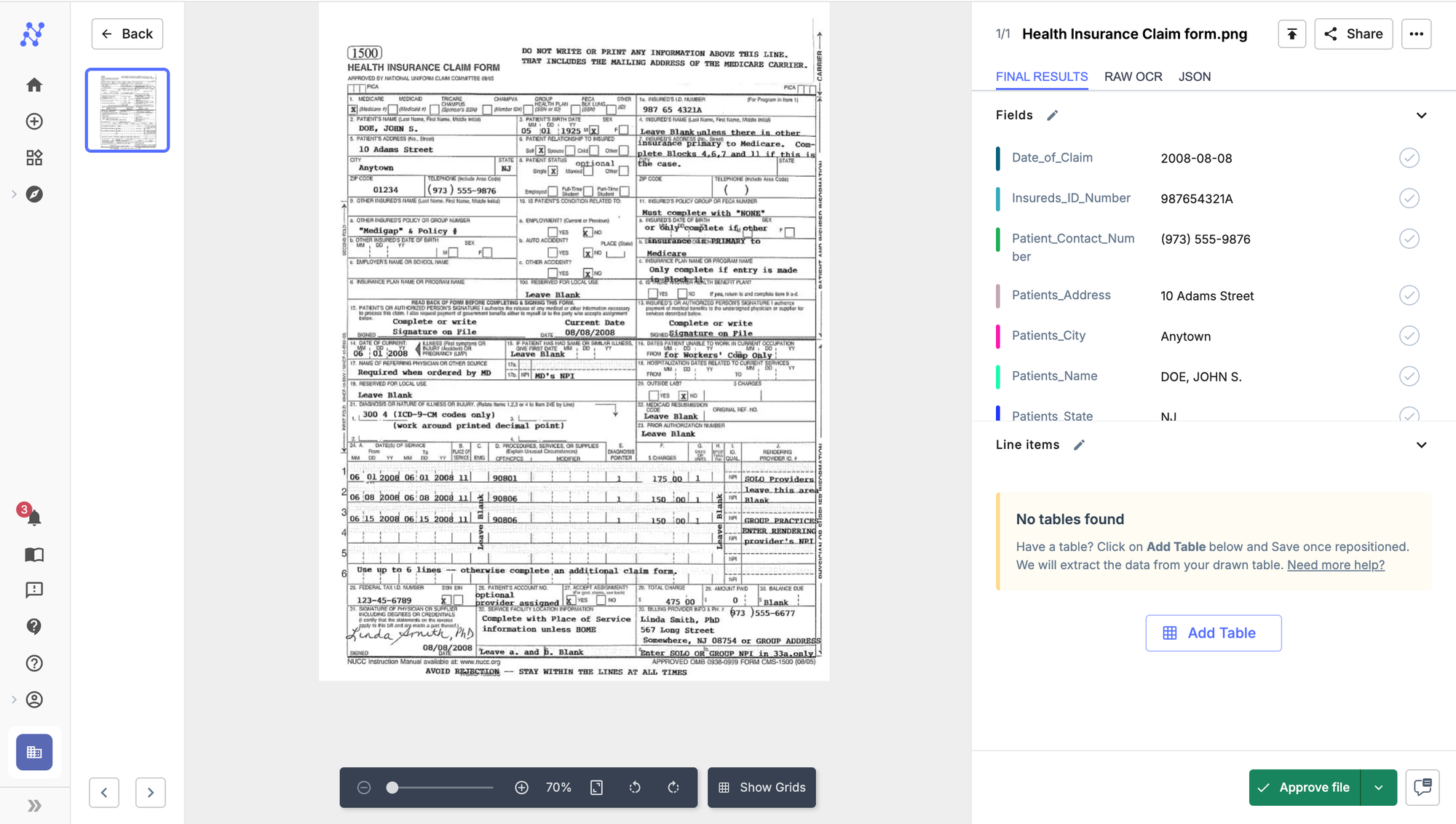

1. Knowledge assortment and aggregation

Underwriters manually collect and enter information from varied sources (e.g. buyer functions, monetary data, and threat assessments).

This course of shouldn’t be solely time-consuming however vulnerable to human error. Furthermore, many paperwork arrive in several codecs, equivalent to scanned PDFs, emails, or handwritten kinds, making it troublesome to course of them shortly and precisely.

Automation utilizing AI-based OCR or clever doc processing (IDP) adjustments this fully. OCR expertise can digitize information from a wide range of paperwork—whether or not they’re in picture, PDF, or textual content codecs, whereas AI-driven extraction programs pull out related particulars contextually, with out counting on pre-set templates. This not solely reduces handbook information entry errors but in addition accelerates the decision-making course of.

Insurers utilizing IDP software program have reported as much as a 90% discount in processing time, permitting underwriters to focus extra on analyzing threat as a substitute of administrative duties.

2. Process administration and workflow automation

Underwriting includes managing a number of duties equivalent to evaluating functions, gathering extra paperwork, conducting compliance checks, and updating coverage phrases. With out automation, underwriters should manually prioritize and handle their workload, typically leading to bottlenecks.

Automation might help streamline process assignments and workflows by utilizing AI to triage duties and assign them primarily based on precedence, complexity, and workload distribution. As an illustration:

- AI can route less complicated functions, equivalent to simple auto insurance coverage renewals or low-risk dwelling insurance coverage insurance policies, to junior underwriters or have them straight by means of processed by the system itself.

- Extra advanced circumstances, like life insurance coverage for people with pre-existing circumstances or high-value properties in flood-prone areas, are routed to senior underwriters.

- Automated programs also can ship reminders for pending duties or compliance evaluations.

By automating process triaging, insurers cut back turnaround instances and enhance process accuracy. This frees up underwriters to give attention to high-value selections equivalent to evaluating non-standard dangers or customizing coverage phrases for distinctive consumer wants.

3. Danger evaluation and pricing

Danger evaluation has historically relied on historic information, equivalent to previous claims, demographic traits, and financial indicators, to judge the chance of future claims. This information is analyzed by underwriters to set applicable premiums.

Nevertheless, this handbook course of is subjective, inconsistent, and gradual, typically resulting in suboptimal pricing selections.

AI and machine studying fashions permit for extra exact threat evaluation by analyzing huge datasets, figuring out patterns, and predicting potential dangers extra precisely. These programs can mechanically alter premiums primarily based on dynamic threat components, equivalent to geographical location, climate patterns, or a person’s well being profile.

As an illustration, AI-supported threat pricing fashions can immediately alter a house owner’s insurance coverage premiums in the event that they transfer from a low-risk to a high-risk flood zone with out ready for handbook evaluate.

This results in higher threat choice and lowered loss ratios. Actually, insurers that use AI for threat evaluation report a 10-15% enhance in income because of improved threat profiling.

4. Compliance

Underwriting additionally includes adhering to regulatory necessities, which may range primarily based on the kind of insurance coverage and the area. Making certain compliance with requirements equivalent to AML/KYC, GDPR, or OFAC is important!

- AI options, like IDP or RPA software program, can automate compliance checks by cross-referencing software information with related rules. For instance, an RPA bot can mechanically examine a consumer’s KYC particulars in opposition to international sanction lists (OFAC) earlier than coverage approval.

- Equally, AI programs can monitor ongoing compliance by flagging any discrepancies between coverage phrases and up to date regulatory necessities.

This automated method ensures that each coverage meets the mandatory authorized requirements with out handbook intervention, decreasing the chance of non-compliance and the related fines.

Core applied sciences driving underwriting automation

Because the insurance coverage trade shifts towards automation, a number of key applied sciences play a pivotal function in reworking the underwriting course of. These applied sciences not solely streamline workflows but in addition improve the accuracy and pace of decision-making, permitting insurers to handle extra insurance policies with fewer sources.

1. AI, Machine Studying (ML), and Clever Doc Processing (IDP)

Synthetic intelligence (AI) and machine studying (ML) are the spine of underwriting automation. When mixed with Clever Doc Processing (IDP), they supply an end-to-end resolution for automating document-intensive workflows, equivalent to these present in underwriting.

In underwriting, AI and ML are used to:

- Predict dangers: AI fashions can assess components like a consumer’s credit score rating, geographic threat (e.g., flood zones), or way of life patterns (e.g., smoking or high-risk occupations) to find out the chance of a declare.

- Automate threat scoring: AI-driven programs can mechanically assign threat scores primarily based on predefined standards, eradicating the necessity for handbook analysis.

- Enhance threat pricing: ML algorithms constantly be taught from new information, bettering their potential to suggest aggressive premiums. This enables insurers to regulate pricing dynamically primarily based on real-time components, equivalent to market traits or adjustments in buyer threat profiles.

- Extract information from advanced unstructured paperwork: IDP powered by AI and ML can extract structured information from advanced paperwork equivalent to claims kinds, coverage functions, medical data, and monetary statements.

- For instance, Nanonets’ IDP system can extract related fields like policyholder particulars, declare quantities, or accident descriptions, decreasing handbook information entry by as much as 90% and dealing with doc processing at speeds far higher than human operators.

The mixture of AI-based OCR and ML helps insurers obtain a big discount in doc dealing with prices whereas making certain information accuracy and consistency.

💡

2. Robotic Course of Automation (RPA)

Robotic Course of Automation (RPA) is one other key expertise that automates repetitive, rule-based duties in underwriting, equivalent to information entry, validation, and coverage issuance. RPA is very helpful for automating the submission consumption course of, the place insurance coverage corporations typically obtain giant volumes of submissions that must be triaged and reviewed.

RPA programs can:

- Automate information transfers: RPA bots can seamlessly switch information between programs, equivalent to from legacy programs like AS/400 or IBM iSeries to trendy cloud-based underwriting platforms, making certain all vital data is available for underwriters. That is particularly useful when integrating with older programs not optimized for contemporary workflows.

- Flag inconsistencies: RPA bots can mechanically flag functions with lacking or inconsistent data, routing them for handbook evaluate, whereas simple circumstances are processed with out human intervention.

- Deal with compliance checks: RPA programs can automate compliance checks, making certain that insurance policies adhere to native regulatory requirements like Solvency II in Europe or the NAIC Mannequin Act within the U.S

💡

By implementing RPA, insurers can course of as much as 10 instances extra submissions in the identical period of time, liberating up underwriters to give attention to extra strategic duties.

Advantages of automating insurance coverage underwriting

Automation delivers tangible advantages to insurers, starting from operational efficiencies to improved buyer satisfaction. Let’s discover these advantages with real-world information and particular examples:

1. Effectivity positive factors

Automation permits insurers to course of functions quicker. For instance, insurers who implement AI-driven underwriting have reported processing instances lowered by as a lot as 70%, with some insurance policies being issued in minutes slightly than days.

Based on a report by McKinsey, AI-driven underwriting can cut back the processing time of advanced functions from days to lower than 24 hours.

2. Improved accuracy

Automation ensures constant, close to error-free information processing, decreasing errors by as much as 75% in areas like information entry and threat calculations.

By utilizing predefined guidelines and AI fashions, insurers can consider each software persistently, decreasing the chance of biased or inconsistent selections.

3. Price financial savings

With automated underwriting, insurers can considerably cut back their reliance on handbook labor and bodily infrastructure for information processing, resulting in decrease operational bills.

Corporations that implement AI and RPA in underwriting processes report operational price financial savings of 30-50%, particularly in high-volume durations the place scaling handbook operations would in any other case require extra workers.

4. Enhanced buyer expertise

With automation, prospects profit from quicker processing instances, extra correct quotes, and a extra customized expertise.

AI programs can tailor premiums primarily based on particular person threat profiles, making certain that prospects get the very best protection at aggressive charges.

- Automated underwriting programs can cut back the time to difficulty a coverage by as much as 60%.

- AI fashions can assess every buyer’s distinctive threat components to supply customized quotes, making prospects really feel that their wants are being met extra exactly.